July 7, 2022

Currency

WASHINGTON: The International Monetary Fund (IMF), Treasury Department currency values in terms of Special Drawing Rights (SDRs). ====================================================================================== July 06, 2022 ====================================================================================== Currency units per SDR SDR per Currency unit ====================================================================================== Currency 5-Jul-22 1-Jul-22 30-Jun-22 29-Jun-22 ====================================================================================== Chinese yuan 0.112825 0.11216 0.112496 0.111938 Euro 0.777582 0.783897 0.782282 0.789041 Japanese yen …

Read More »

July 5, 2022

Banking system

Veteran Bankers Jeffrey Thomas, James Diver to provide business loan services TACOMA, Wash., July 5, 2022 /PRNewswire/ — Columbia Bank, the wholly owned subsidiary of Columbia Banking System, Inc. (NASDAQ: COLB) (“Colombia“), today announced the expansion of its business lending division to Utah with veteran hires Salt Lake City– regional …

Read More »

July 5, 2022

Currency

NNA | Updated: Jul 05, 2022 07:48 STI By Lee Kah WhyeSingapore, Jul 5th (ANI): India’s conservative stance on not encouraging cryptocurrency is quickly vindicated by the negative experiences of various Crypto Funds, the latest being Singapore’s Three Arrows Crypto Fund . Experts say India correctly predicted economic headwinds and …

Read More »

July 2, 2022

Currency

No wonder the government still refuses to commission an economic impact assessment of Brexit; the results would not reflect our exit agreement well. Under these circumstances, it is perhaps surprising that the pound is not under more pressure in the currency markets than it is. So far this year, it …

Read More »

June 30, 2022

Banking system

TACOMA, Wash., June 30, 2022 /PRNewswire/ — Columbia Banking System, Inc. (“Columbia” NASDAQ: COLB) expects to release its second quarter 2022 financial results before market open on Thursday, July 21, 2022. Management will discuss these results on a conference call scheduled for Thursday, July 21, 2022 at 11:00 a.m. Pacific …

Read More »

June 30, 2022

Banking system

TACOMA, Wash., June 30, 2022 /PRNewswire/ — Columbia Banking System, Inc. (“Columbia” NASDAQ: COLB) expects to release its second quarter 2022 financial results before market open on Thursday, July 21, 2022. Management will discuss these results on a conference call scheduled for Thursday, July 21, 2022 at 11:00 a.m. Pacific …

Read More »

June 30, 2022

Currency

An international agency is urging central banks to help strengthen national digital ID systems and make it easier to enforce KYC requirements. The International Monetary Fund (IMF) says in one of its latest reports that digital currency rollout is gradually gaining traction in Sub-Saharan Africa, but countries need to build …

Read More »

June 30, 2022

Banking system

Marketreports.info analysts forecast the latest report on “Global Banking System Software Market (Covid-19) Impact and Analysis by 2030,” according to Banking System Software Report; The Banking System Software Market report covers the overall and all-inclusive analysis of the Banking System Software Market with all its factors that have an impact …

Read More »

June 28, 2022

Currency

Banknote Design and Money Printing Market 2022 this report is included with the Impact of latest market disruptions such as Russian-Ukrainian war and COVID19 outbreak impact analysis key points influencing market growth. In addition, the market for banknote design and currency printing (By Major Key Players, By Types, By Applications …

Read More »

June 28, 2022

Banking system

OTTAWA (ON), June 28, 2022 /CNW/ – Today, the Office of the Superintendent of Financial Institutions (OSFI) released a new Advisory (Clarification on the treatment of innovative secured real estate loan products under Guideline B-20). The Notice complements existing expectations under Guideline B-20which sets out OSFI’s expectations regarding underwriting practices …

Read More »

June 28, 2022

Banking system

Columbia Banking System (NASDAQ:COLB – Get Rating) and Univest Financial (NASDAQ:UVSP – Get Rating) are both finance companies, but which company is better? We’ll compare the two companies based on their dividend strength, analyst recommendations, risk, valuation, profitability, institutional ownership and earnings. Dividends Columbia Banking System pays an annual dividend …

Read More »

June 27, 2022

Banking system

This article is part of a series titled “Supervise the financial institutions of our country. Banking conditions in the United States remained generally strong in the second half of 2021, with strong capital and liquidity, in addition to improving asset quality. This is the conclusion of the Board of Governors …

Read More »

June 27, 2022

Banking system

In May 2022, Big Society Capital (BSC) announced that it was reducing its target rate of return from 4-5% to 1%. While this change is welcome, BSC with its £600m is part of a market it estimates to be worth £6.4bn (2020 data). Commercial banks and other lenders had £464bn …

Read More »

June 26, 2022

Currency

Placeholder while loading article actions There is a lot of turmoil in the forex market about a new “currency war” breaking out, with countries and central banks taking steps to prop up their weakened currencies to offset the strengthening US dollar. The last currency war was a decade ago, but …

Read More »

June 25, 2022

Currency

JCMR released a new industry study that focuses on Global Currency Exchange Software Market and provides in-depth market analysis and future outlook of Global Currency Exchange Software Market . The study covers important data that makes the research document a handy resource for managers, analysts, industry experts, and other key …

Read More »

June 24, 2022

Commercial banks

Anne Juuko, Managing Director of Stanbic Bank Uganda. Picture file Kampala, Uganda | THE INDEPENDENT | Shareholders of banking services companies will start receiving dividends for their investments within a month, for the first time since 2019. Stanbic Bank Uganda and Bank of Baroda will be the first to pay …

Read More »

June 23, 2022

Currency

Media agency Horizon Media said it was working with Comscore on a test to see if Comscore’s local TV measurement data can be used as currency when planning and buying local TV ads. Comscore would offer local buyers an alternative to Nielsen, which has long dominated the ratings industry. Comscore …

Read More »

June 23, 2022

Commercial banks

Kennedy Agyapong, MP for Assin Central The cost of credit remains high in Ghana – Report Development Bank Ghana launched to support specific sectors DBG must deal directly with companies – Kennedy Agyapong Businessman, Kennedy Agyapong has called on commercial banks operating in the country to cut their interest rates …

Read More »

June 21, 2022

Commercial banks

Ghana’s Minister of Agriculture, Owusu Afriyie Akoto, said that although the government had done its best to boost food production by subsidizing the prices of agricultural inputs, such as chemicals, banks had not granted enough loans to complete this effort. This, according to the minister, had made the prices of …

Read More »

June 20, 2022

Currency

The level of Swiss demand deposits fell slightly, data showed on Monday, indicating that the Swiss National Bank has scaled back its foreign exchange market interventions aimed at weakening the Swiss franc. The total level of overnight deposits – cash held overnight by commercial banks with the SNB – fell …

Read More »

June 20, 2022

Commercial banks

The efforts made by the government to boost the agricultural industry in the country did not yield the expected results as the commercial banks did not play the expected role in providing substantial loans to the farmers. Agriculture Minister Dr Owusu Afriyie Akoto said that although the government is doing …

Read More »

June 20, 2022

Banking system

The Covid-19 outbreak has had a devastating effect on the global economy, but Cambodia has managed to maintain good economic stability and the banking system remains strong and solvent to support economic activity, according to a report. In 2021, banking system assets and deposits grew by 18% and 17.7%, respectively, …

Read More »

June 19, 2022

Currency

Today’s exchange rates in Pakistan on June 19, 2022, current dollar rate in Pakistan, latest exchange rates for British Pound, Euro, Saudi Riyal, UAE Dirham, Canadian Dollar , Australian dollar to Pakistani rupees. All rates updated based on free market exchange rates. Today’s exchange rates in Pakistan according to international …

Read More »

June 18, 2022

Commercial banks

The World Bank has said the Central Bank of Nigeria’s low interest lending undermines commercial banks that lend on a risk-adjusted pricing basis and must be curtailed This was revealed by the World Bank in a document titled “Nigeria Development Update (June 2022): The Continuing Urgency of Unusual Cases.’ The …

Read More »

June 16, 2022

Currency

The Russian ruble fell on Thursday after the head of the central bank said most currency controls should be removed. “We had an overlay of currency restrictions. My opinion is that they should be removed, most of them anyway,” Governor Elvira Nabiullina said. The ruble had previously fallen under Western …

Read More »

June 16, 2022

Banking system

Columbia Banking System, Inc. (NASDAQ:COLB – Get Rating) stock price hit a new 52-week low during Thursday’s session. The company traded as low as $27.21 and last traded at $27.24, with trading volume of 2398 shares. The stock previously closed at $28.42. A number of analysts have published reports on …

Read More »

June 16, 2022

Commercial banks

ECONOMYNEXT – Three deaths have been reported due to prevailing weather conditions in Sri Lanka with the onset of the southwest monsoon. Heavy rains are expected to continue in the western, southern and southwestern provinces of the country, officials from the Disaster Management Center (DMC) said. Due to heavy rains …

Read More »

June 15, 2022

Commercial banks

In today’s complex and rapidly changing environment, companies face the same challenge: to grow their business while reducing their expenses. In this blog, we will review five ways commercial banks are approaching these cost savings for the municipal segment. Finding new lending and investment opportunities through municipal market prospecting Finding …

Read More »

June 15, 2022

Commercial banks

zeenews.india.com understands that your privacy is important to you and we are committed to being transparent about the technologies we use. This Cookie Policy explains how and why cookies and other similar technologies may be stored on and accessed from your device when you use or visit the zeenews.india.com websites …

Read More »

June 15, 2022

Currency

There “Currency Exchange Software Market » the research examines the market estimates and forecasts in great detail. It also facilitates the execution of these results by demonstrating tangible benefits to stakeholders and business leaders. each company must anticipate the use of its product in the longer term. Given this level …

Read More »

June 13, 2022

Commercial banks

Maihapa Ndjavera The Bank of Namibia has called on commercial banks to continue to be open and accommodating to local small businesses, and to seek innovative ways to be more inclusive in helping and supporting economic recovery efforts. The remarks were part of Johannes !Gawaxab’s Bank of Namibia (BoN) Governor’s …

Read More »

June 13, 2022

Currency

BAKU, Azerbaijan, June 13. The Central Bank of Iran (CBI) announced the official foreign exchange rate on June 13, Trend reports referring to the CBI. According to the Central Bank of Iran’s exchange rate, 15 currencies rose and 12 fell in price, compared to June 11. According to CBI, 1 …

Read More »

June 10, 2022

Currency

On Friday, India remained on the US Treasury Department’s currency watch list of major trading partners, as Washington placed India along with 11 other major economies that deserve close attention to their monetary practices and policies. macroeconomics.

The countries are China, Japan, South Korea, Germany, Italy, …

Read More »

June 9, 2022

Currency

World trade is dominated by the US dollar, euro, Japanese yen and British pound. The Chinese yuan has a share of about 3%, although China is the largest trading partner for most of the world. As the world’s largest trading nation and at the center of many of the world’s …

Read More »

June 8, 2022

Commercial banks

Cooperative banks will be eligible for more services on an equal basis with commercial banks. Besides tightening limits on home loans, some will now be allowed to lend to commercial real estate. In addition, urban cooperative banks will also be allowed to offer home banking services to their customers. “In …

Read More »

June 7, 2022

Currency

TALLINN, Estonia, June 7, 2022 /PRNewswire/ — Award-winning gaming studio BGaming, a pioneer in crypto-gaming, now supports Crypto SNACK as a currency. This addition puts the SNACK Crypto Token among its impressive portfolio, comprising more than 80 products such as video slots, video poker, lottery, card games and casual games …

Read More »

June 6, 2022

Commercial banks

The main source of bank liabilities is its capital (including cash reserves and, in many cases, subordinated debt). This can come from a domestic or foreign source (corporations and businesses, individuals, other banks and even governments). How much is commercial banking worth? the commercial bank in US market size in …

Read More »

June 5, 2022

Currency

New Jersey, United States – The Global Automatic Currency Detectors Market report examines the current status of the global Automatic Currency Detectors market and industry in detail. All necessary data or information such as market terminologies, concepts, segmentation, key players and other critical information is included in the study. Company …

Read More »

June 5, 2022

Banking system

Sierra Bancorp (NASDAQ:BSRR – Get Rating) and Columbia Banking System (NASDAQ:COLB – Get Rating) are both finance companies, but which company is the best performer? We’ll compare the two companies based on the strength of their profitability, valuation, earnings, institutional ownership, analyst recommendations, risk, and dividends. Dividends Sierra Bancorp pays …

Read More »

June 4, 2022

Currency

A depiction of the Bank of Jamaica (CBDC) central bank digital currency, Jam-Dex logo and slogan. Scammers and other fraudsters will not be able to use central bank digital currency (CBDC) in their illicit activities, the government has promised. Closing the debate on amendments to the Bank of Jamaica (BOJ) …

Read More »

June 2, 2022

Commercial banks

This photo from Kakao Bank shows its debit cards. SEOUL, June 2 (Korea Bizwire) — South Korean financial firms are stepping up efforts to promote their own personas based on the judgment that they would help attract more customers. Among the famous figures in the banking sector is the polar …

Read More »

June 2, 2022

Commercial banks

(Ecofin Agency) – Ghana’s economy is currently affected by high inflation and a weak currency. Commercial banks have resisted so far, but it is uncertain whether their performance will remain as strong as in 2021. Despite the current economic environment, commercial banks operating in Ghana are showing signs of resilience. …

Read More »

June 1, 2022

Currency

(Bloomberg) – Hewlett Packard Enterprise Co. fell about 6% in extended trading after lowering its full-year profit forecast, citing unfavorable currency movements, supply chain disruptions and the impact of leaving the Russian market. Earnings, excluding certain items, will be $2.10 per share in the year, seven cents per share lower …

Read More »

June 1, 2022

Banking system

This content was provided by a business partner. I have seen an increasing number of customers asking about overseas payments. Recently, this has been driven by a number of particularly difficult situations that have made using the formal banking system either difficult or impossible. Often, decisions must be made at …

Read More »

May 31, 2022

Banking system

London-based cross-border payments platform xpate has launched a new core banking solution to simplify merchant payment system integrations with multiple acquirers. xpate launches its own core banking platform Xpate says its cloud-based solution will give merchants “the widest possible access” to integrated payment processing, real-time data analytics and transaction routing …

Read More »

May 30, 2022

Currency

NFC PAYMENTS: The palm-sized device is a combination student card, phone, and digital yuan hard wallet Students attending Hainan Lu Xun Middle School in the Chinese city of Sanya are the first in the country to test a yuan-denominated digital wallet device that allows them to make payments to designated …

Read More »

May 29, 2022

Commercial banks

The bank’s most significant liabilities are capital (mainly cash reserves and, in some cases, subordinated debt) and deposits. It can be obtained from domestic or foreign sources (companies, businesses, individuals, other banks and even governments). What is the greatest responsibility of a commercial bank? The bank is most vulnerable to …

Read More »

May 28, 2022

Currency

New Jersey, United States – Verified Market Reports has released the latest competent intelligence market research report on the Currency Counting Machines market. The report aims to provide an in-depth and accurate analysis of the Currency Counting Machines market, taking into account market forecasts, competitive intelligence, technical risks, innovations, and …

Read More »

May 27, 2022

Banking system

The bank’s liabilities include its capital (including cash reserves and, occasionally, subordinated debt) and deposits. Foreign governments, companies and individuals may also provide (although not directly related). What is the main responsibility of the commercial bank? Deposits are the most common type of liability for commercial banks. Deposits are a …

Read More »

May 26, 2022

Currency

The sudden and rapid rise of Bitcoin, Ethereum, and other cryptocurrencies over the past few years, coupled with the potential applications of blockchain and distributed ledger technologies in virtually every industry, has generated a wave of innovation, disruptive businesses and a modern digital economy. With this explosive growth, new legal …

Read More »

May 26, 2022

Banking system

Hungary’s banking system was in a “state of readiness” as it faced a sharp increase in risk due to the war in Ukraine, and the sector’s capital and liquidity buffers ensure that lenders will be resilient even if the conflict extends, the National Bank of Hungary (NBH) said in a …

Read More »

May 25, 2022

Commercial banks

Changes in banking are now happening at an accelerating pace, a bank is now seeing changes in a year that took decades to materialize. These changes are reflected in loan-to-deposit ratios as well as what is on banks’ balance sheets, which in turn influences bank performance. Banking sector quarterly net …

Read More »

May 24, 2022

Currency

BEIRUT (AP) — Lebanon’s currency hit a new low on Tuesday as deep divisions in the newly elected parliament raised fears that political paralysis could further exacerbate one of the worst economic collapses in history. The legislature elected on May 15 showed no clear majority for any group and a …

Read More »

May 21, 2022

Banking system

Columbia Banking System (NASDAQ:COLB – Get an Assessment) was downgraded by Zacks Investment Research from a “buy” rating to a “hold” rating in a research report released Friday to clients and investors, Zacks.com reports. According to Zacks, “Columbia Banking System, Inc. is a registered bank holding company whose wholly-owned subsidiary, …

Read More »

May 19, 2022

Currency

Sri Lanka’s central bank said it would reduce the maximum amount of foreign currency individuals can own from $15,000 to $10,000 and penalize anyone who holds it for more than three months By Bharatha Mallawarachi Associated Press May 19, 2022, 3:45 p.m. • 3 minute read Share on FacebookShare on …

Read More »

May 19, 2022

Currency

The Uganda Security Printing Company (USPC) yesterday started construction of the security printing factory in Entebbe. USPC was established on October 4, 2018 as a joint venture between the Ugandan government and a German consortium Veridos. The partnership aims to revamp the Uganda Printing and Publishing Corporation (UPPC) by redesigning, …

Read More »

May 18, 2022

Banking system

WASHINGTON — When it comes to major market turbulence, banks escaped last week’s TerraUSD crash largely unscathed. Terra and its corresponding crypto coin Luna fell last week, losing almost all of their value and sending the crypto market into a selloff. It was an existential moment for crypto proponents and …

Read More »

May 18, 2022

Currency

A study shows that 90% of interrogates central banks around the world are exploring the future issuance of central bank digital currencies (CBDCs). Blockchain.News interviewed industry experts to find out the prospects for Hong Kong’s digital currency and its potential adoption. The outlook for e-HKD In a recent discussion paper …

Read More »

May 17, 2022

Banking system

John Ryan, a passionate advocate of dual banking and a driving force as chairman and chief executive of the Conference of State Banking Supervisors, where he worked for 25 years, died suddenly late Monday night at his home in Washington. He was 58 and died of natural causes, said CSBS …

Read More »

May 14, 2022

Currency

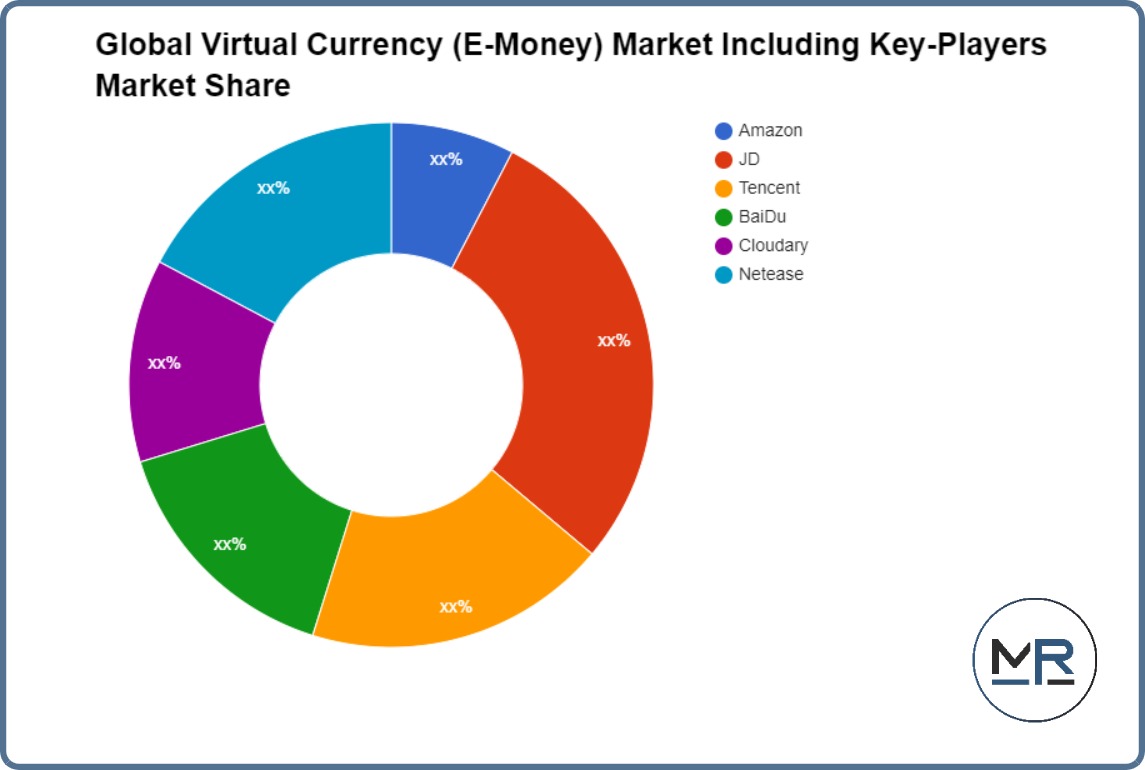

Exclusive Virtual Currency (Electronic Money) Market Research Report provides in-depth analysis of market dynamics across five regions such as North America, Europe, South America, Asia- Pacific, Middle East and Africa. Segmentation of Virtual Currency (Electronic Money) Market by Type, Application and Region has been done based on in-depth market analysis …

Read More »

May 13, 2022

Currency

To print this article, all you need to do is be registered or log in to Mondaq.com. On May 6, 2022, the United States Department of Treasury’s Office of Foreign Assets Control (“OFAC”) designated crypto mixer Blender.io as a Specially Designated National (“SDN”), marking the first time a virtual currency …

Read More »

May 10, 2022

Currency

PITTSBURGH, May 10, 2022 /PRNewswire/ — “My uncle owns a gas station and a lot of paper money changes hands. I thought there should be a way to sanitize money to prevent the spread of germs,” said an inventor, Louisville, Ky.“So I invented the CASH DISINFECTANT. My design eliminates the …

Read More »

May 9, 2022

Currency

The Venezuelan government is now focusing its action on trying to establish the bolivar as the reference currency for purchases in the country. According to several economists, this could be a risky bet in a country which has just emerged from hyperinflation and which still suffers from high levels of …

Read More »

May 8, 2022

Commercial banks

Doha: Qatar’s banking sector continued to record robust growth in March as the country’s commercial banks recorded an increase in deposits and credit facilities, according to the latest data released by the Planning and Statistics Authority (PSA). According to the report, cash equivalents including commercial bank deposits in Qatar stood …

Read More »

May 8, 2022

Banking system

Surrey Bancorp (OTCMKTS:SRYB – Get Rating) and Columbia Banking System (NASDAQ:COLB – Get Rating) are both finance companies, but which company is the best performer? We’ll compare the two companies based on the strength of their profitability, valuation, institutional ownership, dividends, analyst recommendations, risk and earnings. Dividends Surrey Bancorp pays …

Read More »

May 7, 2022

Currency

The Reserve Bank of Zimbabwe says deterrent sanctions are needed if the country is to deal with currency manipulators once and for all. Over the past two years, the country’s macro-economic environment has been besieged by economic saboteurs, who have manipulated the local currency to the chagrin of Zimbabweans. The …

Read More »

May 6, 2022

Banking system

SMI offers a complete study of the “Islamic banking marketwith all-inclusive insights into vital factors and aspects that impact the future growth of the market. The report’s segmentation analysis has provided the performance of different product segments, applications, and regions in the Islamic Banking System market. This report covers the …

Read More »

May 6, 2022

Banking system

The banking system remained broadly sound, with strong capital and liquidity and improving asset quality in the second half of 2021, according to the Federal Reserve’s latest supervisory and regulatory report released today. The Fed said risk monitoring will continue for the potential effects of the pandemic and new geopolitical …

Read More »

May 6, 2022

Banking system

Banking system credit growth recorded a significant recovery at the start of FY23, with credit growth of 11.2% year-on-year as of April 8, 2022, compared to 5.3% year-on-year during FY23. same period in April 2021, and the highest since July 2019. India Ratings and Research (Ind-Ra) estimates that while the …

Read More »

May 5, 2022

Banking system

This discussion should be read in conjunction with the unaudited Consolidated Financial Statements of Columbia Banking System, Inc. (referred to in this report as "we", "our", "Columbia" and "the Company") and notes thereto presented elsewhere in this report and with the December 31, 2021 audited Consolidated Financial Statements and its …

Read More »

May 5, 2022

Currency

New Jersey, United States – Complete analyzes of the most dynamic Currency Counting Machine Market provide information that helps stakeholders identify opportunities and challenges. The 2022 markets could be another big year for currency counting machines. This report provides an overview of the company’s activities and financial situation (a company …

Read More »

May 5, 2022

Banking system

Stratagem Market Insights recently published a market research report titled “Islamic banking market » Size, Status and Forecast 2022-2028”. The research study is a good resource to have for keeping abreast of the latest developments and future advancements in the global Islamic Banking market. The report authors have used the …

Read More »

May 5, 2022

Banking system

The surprise rate hike by the RBI signaling a reversal in the interest rate cycle will weigh on credit growth in the banking system, which was showing signs of recovery with growth of 11%, according to a report on Thursday. The tailwinds supporting a recovery in credit growth will be …

Read More »

May 5, 2022

Banking system

By PTI MUMBAI: The surprise rate hike by the RBI signaling a reversal in the interest rate cycle will weigh on credit growth in the banking system, which was showing signs of recovery with growth of 11%, according to a report on Thursday. The tailwinds supporting a recovery in credit …

Read More »

May 4, 2022

Banking system

On May 4, 2022, the Federal Reserve announced a plan to reduce the size of its balance sheet. At $9 trillion and ten times more than before the 2008 financial crisis, the Fed’s asset accumulation has helped reduce borrowing costs across the economy, push up share and real estate prices …

Read More »

May 3, 2022

Currency

A fourth member of an organized crime group has been jailed for conspiring to provide more than £12million worth of counterfeit banknotes.

Farningham resident Andrew Ainsworth, 61, was convicted of conspiracy to produce counterfeit money following a trial at Woolwich Crown Court in March 2022. He was sentenced to …

Read More »

May 3, 2022

Banking system

The Philippine banking system saw total deposits increase by 9% to 16.2 trillion pesos in 2021, more than the 14.9 trillion pesos recorded in 2021 as the economy recovered from the COVID-19 pandemic , said the Philippine Deposit Insurance Corp. (PDIC). Tuesday. In a new statement, the PDIC said the …

Read More »

May 2, 2022

Commercial banks

Data shows that 11 Nigerian banks in 12 months incurred more than N536.09 billion on salaries and wages of their staff. The figure was obtained from the annual results of banks submitted to the Nigerian Stock Exchange. Banks surveyed include Eco Bank, First City Monument Bank (FCMB), Fidelity Bank, Guaranty …

Read More »

May 1, 2022

Currency

The Indian government is exploring “multiple commercial use purposes not just financial inclusion” for its central bank digital currency. India’s finance minister has clarified that the aim is for the digital rupee, which will be backed by the Reserve Bank of India (RBI), to be issued by 2023. India’s Finance …

Read More »

April 30, 2022

Banking system

TEHRAN – Iranian Finance and Economic Affairs Minister Ehsan Khandouzi on Saturday unveiled a new package of measures for the management of the country’s banking sector, IRNA reported. In line with the new year’s motto which is “knowledge-based and job-creating production”, the mentioned package includes policies and strategies that are …

Read More »

April 30, 2022

Commercial banks

Banks can include government securities worth up to 16% of their NDTL in their LCR calculations, up from 15% under previous guidelines. Access today Sign up for a 2 week free trial and get instant, unrestricted, unrestricted access to Regulation Asia. FREE TRY Already taken your free trial? Contact our …

Read More »

April 30, 2022

Banking system

KARACHI: The State Bank of Pakistan (SBP) on Friday injected a massive 3.565 billion rupees over a seven-day period at 12.30% through a reverse repurchase agreement, as liquidity was distorted on the Money Market. The SBP separately also conducted a Sharia-based open market operation (OMO) on the same day, injecting …

Read More »

April 29, 2022

Currency

Editorial Note: We earn a commission on partner links on Forbes Advisor. Commissions do not affect the opinions or ratings of our editors. Our currency conversion calculator converts over 200 currencies and rates are updated every five minutes. Among the currencies available, our calculator converts Mexican pesos, Indian rupees, Russian …

Read More »

April 29, 2022

Banking system

ISLAMABAD: The Federal Shariah Court (FSC) on Thursday gave the government five years to establish an Islamic and interest-free banking system in the country because the economic system of an Islamic country like Pakistan should be interest-free. Judge Dr Syed Muhammad Anwar read out the verdict which was reserved by …

Read More »

April 29, 2022

Banking system

ISLAMABAD: The Federal Court of the Shariat (FSC) has declared that the prohibition of Riba is complete and absolute in all its forms and manifestations according to the injunctions of Islam; therefore asked the government to implement its decision by December 31, 2027. The FSC Plenary Panel, comprising Chief Justice …

Read More »

April 28, 2022

Banking system

The Federal Shariah Court (FSC) on Thursday announced a verdict in a long-pending Riba (interest) case, declaring the prevailing interest-based banking system against Shariah and ordered the government to facilitate all lending in under an interest-free system. . In its long-awaited verdict, the court ruled that the federal and provincial …

Read More »

April 28, 2022

Commercial banks

The banking sector in Qatar showed resilience and recorded growth in February. Commercial banks in Qatar saw an increase in deposits and credit facilities year-on-year in February 2022 according to data from the Planning and Statistics Authority.Public sector deposits stood at QR 279.5 billion in commercial banks in February 2022, …

Read More »

April 27, 2022

Commercial banks

With so many lenders vying for commercial real estate transactions, commercial banks have had to become more flexible and offer financing structures that match their rivals. KeyBank, for example, offers financing formulas similar to those offered by private equity firms and life insurance companies. This includes on- and off-balance sheet …

Read More »

April 26, 2022

Commercial banks

The results of the audit of the annual report for the financial year 2020/21 indicate that applications from commercial banks have been received by the Bank of Tanzania (BoT) for the assessment, credit assessment assessment of l financial institution and project due diligence was performed as required, however, guarantees were …

Read More »

April 24, 2022

Currency

Data from the Central Bank of Egypt (CBE) shows that the net foreign asset (NFA) position fell sharply from $13.7 billion to $5.1 billion in March, amid outflows from capital from non-residents triggered by the situation in Ukraine. Capital flight has raised fears of further currency volatility. In addition, capital …

Read More »

I Have 50 Dollars

I Have 50 Dollars